This article may contain personal views and opinion from the author.

Never mind what the regulators have been hinting, I really cannot imagine that T-Mobile customers are all that excited about a possible merger with Sprint either.

On one side, you have a glistening beacon of competition which, as the smallest of the "big four," has managed to transform the wireless industry in the United States in less than a year. On the other side, you have a hemorrhaging patient being stitched together with a hodge-podge of different networks.

When it comes to making money, I’m on the side of “more.” For Deutsche Telekom, the company would be serving its shareholders pretty well if it manages to get $40 billion-ish for its stake in T-Mobile USA. If Masayoshi Son wants to spend SoftBank’s money on such a venture, have at it. In the world of mergers and acquisitions, and big business, I really do not have much of a problem with such deals.

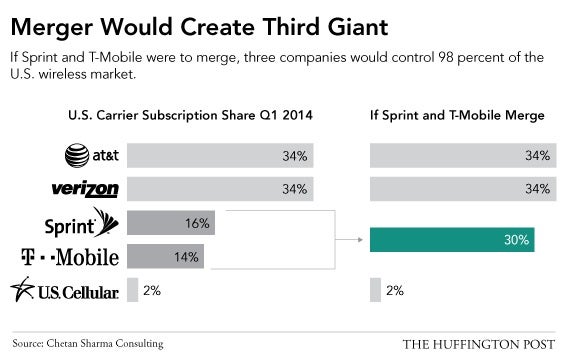

Competition among three giants

Control of the market consolicates dramatically

As someone who digs competition however, I am not thrilled with the idea. As someone who has been a customer of both these carriers (as well as Verizon and AT&T), albeit for short periods of time, I am really not thrilled with the idea. As someone looking in from the outside at the relative cultures of two companies, I am really, really not thrilled with the idea of a T-Sprint or SprinT-Mobile or whatever they call it.

Recommended For You

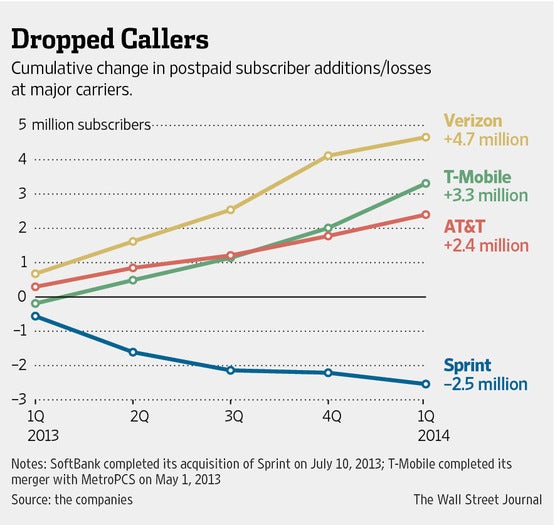

Verizon and AT&T control two thirds of the US mobile market, and basically 100% of the profits. If Sprint and T-Mobile combine, none of that changes. The two companies would be larger, but T-Mobile, despite its amazing subscriber growth, is barely making any money, or none at all, and Sprint, just isn’t making any money or gaining any customers and hasn’t been for years. So, in gaining T-Mobile, Sprint simply gains more overhead.

Employees of T-Mobile and Sprint should update their resumes

Speaking of overhead, what happens when a company is contending with too much overhead? You lay people off and you close down stores. While it would be technically inaccurate to say that where there is a Sprint store there is also a T-Mobile store, it is not inaccurate to say that there are plenty of places where a combined company will have wholly duplicated operations at common locations and regions when only one will be needed. Where there are 10 or 20 call centers, you will only need a fraction of that. Property managers and tower technicians, they’ll feel the pinch too. Two sales teams covering the same geographic territory, no more. So, regardless of what you hear, yes indeed, there will be a lot of people losing their jobs. Employees are the most expensive cost on any company's normal balance sheet.

A network of 31 flavors and no new coverage

Then there is the matter of how the combined company would continue growing its customer base. Even with John Legere at the helm to be the business evangelist and let’s assume that current T-Mobile CTO Neville Ray, who orchestrated the spectrum changeover with MetroPCS, how would a combined company effectively manage Sprint’s CDMA, FD-LTE, TD-LTE, left-over WiMAX network, and build a base on top of T-Mobile’s GSM/HSPA and LTE network?

One thing this merger is not about is coverage. Neither carrier has much of an advantage over the other. Both incumbent networks were built from the ground up after the PCS (1900MHz) auctions in the 1990s. One could make the argument about spectrum, T-Mobile holds more “low-band” spectrum (less than 1000MHz) than Sprint, but given that both networks are a virtual overlap, regulators are certainly going to mandate some significant divestiture of licenses in major markets, particularly in California, Texas, and Florida, three of the biggest states in the Union.

Doing a T-Mobile/MetroPCS strategy, a-la migrate users to one network, then shut down the other, is possible, but it would be a daunting undertaking. It was feasible with MetroPCS because the carrier had a little less than 10 million subscribers. T-Mobile was able to accomplish the feat ahead of schedule, while giving itself about 2 years to do the job. Migrating 50 million subscribers in one direction or the other would be cost prohibitive, and very slow unless you just starting giving truckloads of equipment away (thus pressuring further the non-existent profits in either company).

Auction rules become moot

What about the auction in 2015? All that beach-front 600MHz spectrum is going to be up for grabs. The FCC even wrote in rules favoring smaller carriers in markets where AT&T and Verizon have significant holdings already, just as what T-Mobile, Sprint, and the Competitive Carriers Associations lobbied for. It is indeed interesting that the regulators wrote in that those favors would be pretty much null and void if a “significant transaction” were to be announced. So, it would seem that John Legere and Dan Hesse weren’t standing up for the “little guy” despite all their lobbying of the FCC to get the auction rules written in.

Kiss market scalability goodbye

I may be seeing all this from the outside-looking-in, but it all looks like a tangle to me. Instead of four carriers controlling 98% of the market, you would have three. That’s less competitive. The resulting fourth largest carrier would be US Cellular with 5 million customers. In fact, if I were to buy US Cellular, C Spire, nTelos, Cellcom, Alaska Wireless, SouthernLINC, Bluegrass Cellular, and Appalachian Wireless, the next biggest carriers in line, the combined company would still be smaller than MetroPCS was when it was acquired by T-Mobile, with just 7.6 million customers. There would be no more scalability in the market if these two companies merge.

It may be a third giant, but it would be a stagnant one, and would not have the momentum of growth that AT&T and Verizon have been able to generate, T-Mobile's gains are canceled by Sprint's losses

A strange attraction

Even with John Legere at the helm, there is a much different owner in the picture, Masayoshi Son versus Deutsche Telekom, and given the far more conservative hand Son has played thus far with Sprint, versus what many expected, I am not convinced the two would get along all that well. Moreover, neither carrier gains any physical coverage. The end result is a carrier with north of 80 million customers, a heap of debt, and a network that is compiled of a whole bunch of incompatible standards. Legere’s vision and flexibility is offset by Sprint’s inflexibility, and T-Mobile’s subscriber growth is offset by Sprint’s losses. Also, remember my aforementioned view of job cuts, expect to see all the wrong people in the middle lose their jobs as relative teams jockey to justify their (continued) existence (you can look at just about any Dilbert comic as a reference).

When these rumors about a possible merger first surfaced, I reasoned that given track records, it should be Sprint putting itself up for sale. John Legere has arguably not made a bad move in his short time at the helm of T-Mobile USA, though the subscriber gains need to turn into profits or it is all for naught. Sprint, on the other hand, has been making bad decisions since it bought Nextel.

This deal is good for a few key people and a couple of companies. Dan Hesse and John Legere, as CEOs, along with a group of key executives, will get handsome paychecks from the deal (that’s good, I have no problem with people making money). The major shareholders of T-Mobile USA, most of which is Deutsche Telekom, and subsequently, its shareholders, are well served in any transaction.

Interestingly, it could be shareholder disposition that might prove to be an impediment to SoftBank’s cash flow. SoftBank is a major owner of Alibaba, who is basically to Asia what Amazon is to the US. Alibaba is gearing up for an IPO that is going to raise a significant amount of money. However, Alibaba has been rather quiet about several details ahead of remaining regulatory filings that investors are interested in. The details are too far off topic, but Alibaba’s own acquisitions, and the way the company projects financial results for each business unit, coupled with relative silence about the make-up of other partners involved in the company and their voting power in Alibaba after it goes public. If anything were to hamper what is expected to be a record setting IPO, that will certainly have an impact on Masayoshi Son’s enthusiasm (or ability) to pay a premium for T-Mobile.

It makes sense - just like trying to make a soup sandwich

This is one of the ads that Sprint ran in its campaign to stop the AT&T buyout of T-Mobile - anything different this time?

T-Mobile has been an invigorating game changer in what is a nearly saturated US market. How that dynamic alone may be affected by a T-Mobile-Sprint merger is something that should be examined by regulators no matter how much of the store Masayoshi Son promises to give away. Moreover, do not expect AT&T to take such a measure lying down. Sprint proved to be a massive thorn in AT&T’s side in its attempt to buy T-Mobile a few years ago, and that merger, though disliked by consumers, made a lot more sense. Don't be surprised if a lot of drama unfolds following any announcement by T-Mobile and Sprint.

The final judge in all this will of course be the customers. The problem is that the resultant merger would indeed mean they have fewer choices to consider if they want to make a switch. If this deal goes through, it's a total insiders deal. It also proves that Masayoshi Son never intended to actually try and turn Sprint around. From every other angle it looks like they're trying to make a soup sandwich. All we're going to get is soggy bread.

Our new coffee table book, Iconic Phones, is a stunning visual tribute to the legends in the world of phones, featuring exclusive high-resolution photography, stories, quotes and fun trivia. Save 10% by using this code at checkout: XMAS10. Offer lasts until 1 January 2026.

Maxwell Ramsey has made significant contributions to PhoneArena through his detailed reporting on technology policy and advancements, such as wireless charging standards and FCC regulations, helping demystify complex topics for a broad readership.

COMMENTS (62)

COMMENTS (62)

All comments need to comply with our

Community Guidelines

PhoneArena Community Rules

A discussion is a place, where people can voice their opinion, no matter if it

is positive, neutral or negative. However, when posting, one must stay true to the topic, and not just share some

random thoughts, which are not directly related to the matter.

Things that are NOT allowed:

Off-topic talk - you must stick to the subject of discussion

Offensive, hate speech - if you want to say something, say it politely

Spam/Advertisements - these posts are deleted

Multiple accounts - one person can have only one account

Impersonations and offensive nicknames - these accounts get banned

To help keep our community safe and free from spam, we apply temporary limits to newly created accounts:

New accounts created within the last 24 hours may experience restrictions on how frequently they can

post or comment.

These limits are in place as a precaution and will automatically lift.

Moderation is done by humans. We try to be as objective as possible and moderate with zero bias. If you think a

post should be moderated - please, report it.

Have a question about the rules or why you have been moderated/limited/banned? Please,

contact us.

![Some T-Mobile users might be paying more starting March [UPDATED]](https://m-cdn.phonearena.com/images/article/176781-wide-two_350/Some-T-Mobile-users-might-be-paying-more-starting-March-UPDATED.webp)

Things that are NOT allowed:

To help keep our community safe and free from spam, we apply temporary limits to newly created accounts: