Making money in the mobile industry is not an easy task. It is currently at the forefront of the consumer electronics lust, and the breakneck pace of innovation in the last few years has caught some of the incumbents totally unprepared. Profit margins used to be relatively thin, compared to the old guard of oil, financial or military-industrial complex companies, save for a few value added propositions like RIM or HTC, while Nokia was synonymous with cell phones for many people around the world.

Who knew four years ago that Apple's rounded thingy that looked like a soap box with a touchscreen and only one button will disrupt the industry like few inventions before and none so fast. Now Nokia and RIM are on a transitional path from which they might never emerge like the companies they were before, while industry ex-stalwarts like Motorola and Sony Ericsson spent this period mostly in the red.

Perhaps the main reason was that Apple is a computer, not a cell phone company, so it was trying to recreate its trademark seamless user experience in its first mobile phone as well, capitalizing on a few years of iPod sales lessons. Most probably even Steve Jobs didn't foresee that Apple's iPhone will actually fulfill a dire need for an easy to use pocket computer you can always carry with you and stay connected, which was evidently dormant in a lot of us.

Recommended For You

Anyway, we might argue until we are blue in the face about the yardstick to measure achievements in the industry, but these are not oil companies providing a necessity, or investment banks, looking for the next sucker. These are companies that manufacture electronics for the fickle consumer market, who is their ultimate judge, that is why we combed through the financial statements of the eight most visible cell phone companies. What better way to illustrate the game of musical chairs that the mobile phone industry has been playing for four years now, than to trace how are people voting with their hard-earned cash in the times of the Great Recession?

Methodology

We took the quarterly handset business results Q1 2007-Q1 2011, and extracted sales, operating profit and margin, total number of handsets sold, and average selling prices. Most of these companies don't report net results from the phone divisions, so we went with their operating profits – moreover, we are dealing with international companies, which get taxed differently. Samsung and LG don't report the results of their handset divisions separately in the annuals, but they do it in the quarterly earnings presentation slides, so that's what we used. Apple doesn't report its margins for the iPhone or iPad, but a pretty close approximation can be obtained by the gross profit and the operating expenditures share, with the presumption its percentage is similar to the one reported relative to Apple's general sales.

We also evened out the reporting periods, since some companies, like RIM, have the first quarter ending in May, for example. The results in currencies that don't fluctuate much to the dollar we converted by the average annual exchange rate for that year (Samsung, LG, HTC), while the results in EUR (Nokia, Sony Ericsson) we converted quarter by quarter, using the average EUR/USD exchange rate reported by Nokia in its quarterly results. Finally, we added the iPad separately, just for kicks.

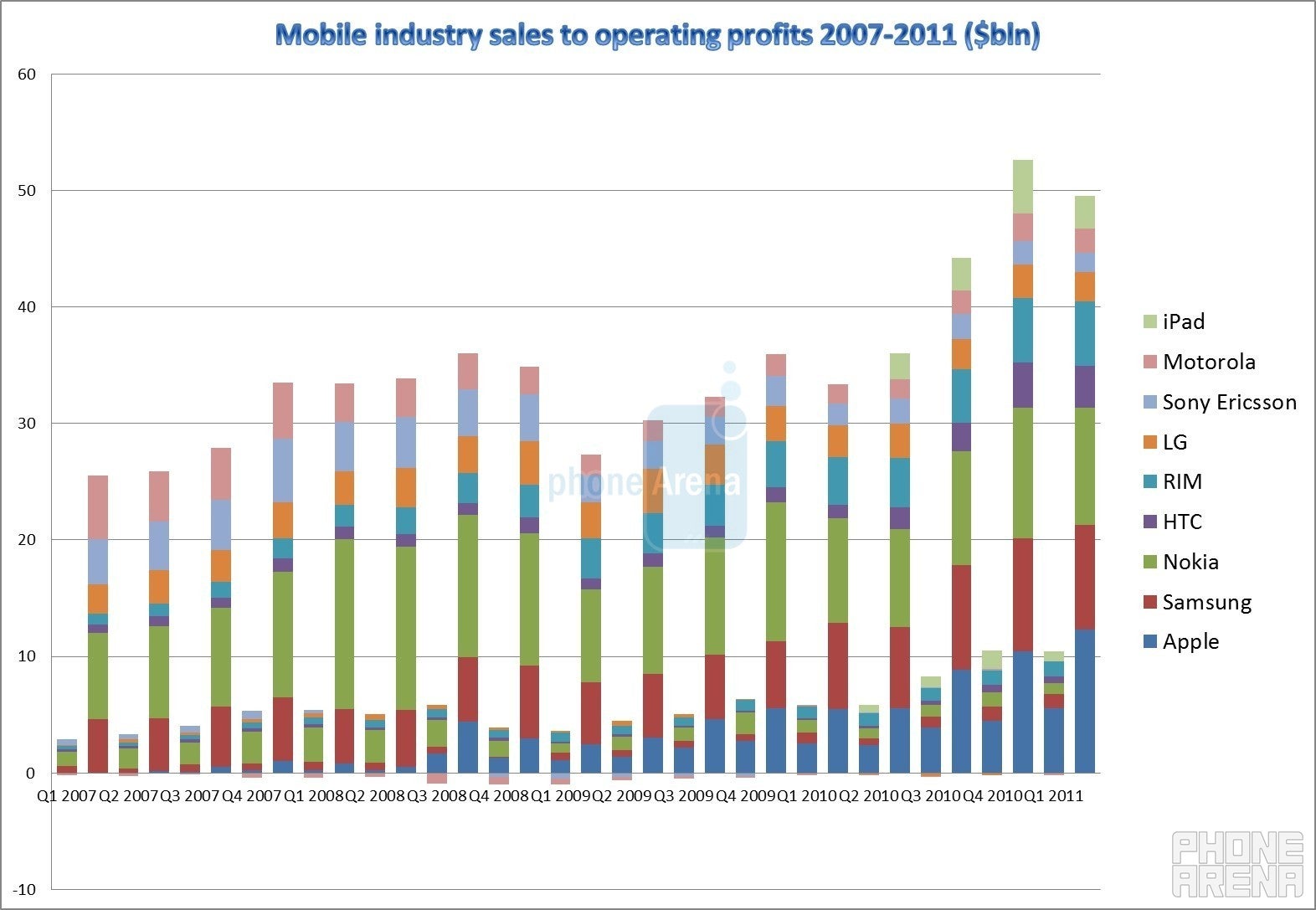

While we were creating the resulting spreadsheet with more than 600 entries the numbers started to get pretty revealing, but when we put it all on a timeline in chart form, the level of disruption that occurred in this relatively short four-year period was even more glaring.

Sales, operating profits, margin

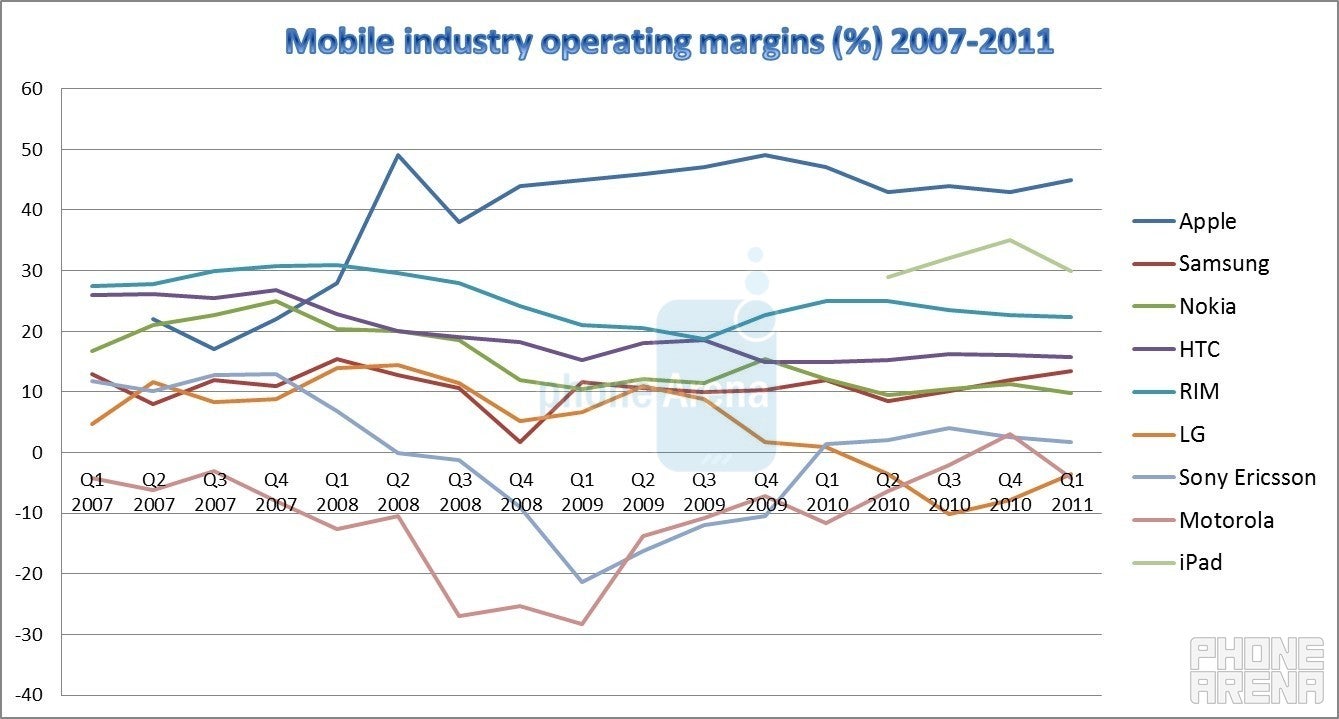

What can be easily seen from the chart below, is that Apple's operating profit (OP) converged with the declining profit of the number one cell phone manufacturer by volume Nokia around the end of 2008, and then really took off, with the line becoming almost parabolic after the iPhone 4 was introduced with its new design, high-res display and a decent camera in 2010.

The other major observation is that Android has been a lifeboat for many of the cell phone industry laggards. Due to the perfect storm of a financial crisis in 2008 when Lehman collapsed, the iPhone popularity taking off, and the appearance of Android, companies that were churning feature phones with rather decent margins, started diving deep into the red at that time. It took until the first months of 2010 for them to recover, and only after they started offering high-margin handsets with Android, some approached breakeven (Sony Ericsson, Motorola), and others started seeing a nice lift in handset profits (HTC, Samsung). LG, which didn't move to Android until Q3 2010, resulting in the LG CEO exit, started seeing diminishing losses with the introduction of Android handsets like the popular LG Optimus One, and now with industry firsts like the LG Optimus 2X or the Optimus 3D. Still, LG recently cut its sales target quite a bit, indicating troubled times ahead for the world's 3rd largest cell phone maker.

Operating profit in itself doesn't say much, unless we compare to sales, and the chart below shows why Apple, RIM and HTC are taking the profit lead. Apple's profit margin hovered around the 20th percentile when the iPhone was introduced, to reach the stratospheric 40+ percentage rates nowadays. Due to its unique service offerings, RIM is also enjoying 20-30% operating profit margins, despite offering handsets that can technically be considered lackluster when compared to the best of the competition, which comes to demonstrate how valuable are any unique services you are offering together with your handsets.

HTC is the other company that has been doing things right all along, as we wrote in 2008 – it nailed the magic formula to enjoy 20+ % profits before Apple, by producing only high-margin innovative smartphones, since the dawn of Windows Mobile. Had Microsoft made WinMo what WP7 is now earlier, HTC could have exploded, too, despite lacking Apple's clout and brand recognition. Today, thanks to its high-end Android handset it enjoys both, and the average selling price of its phones is second only to Apple's, recently making HTC's chairwoman Cher Wang the richest person on an island of millionaires like Taiwan. As seen in the chart below, however, HTC's margin has been steadily diminishing, coming down to 16-18% in the last few quarters, which is, however, compensated by a strong demand for the company's handsets.

Samsung reported its highest operating margin of 13.5% in Q1, while it is usually hovering in the 7-11% range. This is undoubtedly due to things like the innovative technologies it introduced with the Super AMOLED display and the Hummingbird chipset last year in a high-margin Android handset. We expect these numbers to receive a boost with unique propositions like the Samsung Galaxy S II this year as well.

What is most astonishing, however, is that Apple currently has only 5% of the market, but see all that blue in the OP column in the chart above for Q1 2011? It rakes in more than half of the industry's operating profit that is up for grabs, that’s how seismic the iPhone disruption was. Due to the stratospheric average selling price of its units compared to the other players, its profit margin of more than 40% for the iPhone is outstanding compared to, say, the low teens for Samsung’s whole lineup.

Average selling price, number of handsets sold, market share

And here we arrive at the all important metric of Average Selling Price (ASP) in the cell phone business. That's the amount each handset a company produces gets sold for on average via all channels – carriers, retail, and so on. We can write volumes about the added value people see in handsets made by Apple, RIM or HTC, which make a phone for roughly $200 in components and assembly (even less for RIM), plus some R&D, marketing and administrative expenses, and then sell it retail for respectively $600+, $304 or $359 in the first quarter of this year. Apple is looming particularly large here, prepaying suppliers like Samsung in huge amounts, or loaning them money for specialized equipment, thus corralling whole component markets for itself, achieving rock bottom component prices which nobody else can match. One of Apple's issues actually is limited capacity in the supply chain to meet the demand for its gadgets, resulting in the recent delay of the next iPhone, which is turning out quite difficult to manufacture, and had both Foxconn and OmniVision huffing and puffing about the unbearable difficulties of being Apple's supplier or assemblyman.

Until recently Apple was selling its vertically integrated product in a monopolistic-like vacuum. There was just no way to quickly copy the combination of enticing hardware and user experience, with the enormous potential of 500 000+ pre-selected apps at your fingertips. People wanted the most intimate of their gadgets – their phone - to offer effortless individuality, and that’s what Apple went for – creating a status symbol, as usual. This resulted in the outrageous $600+ ASP of the iPhone, raking in Apple's huge revenues.

As can be seen from the charts - total handsets sold 2007-Q1 2011, and the ASPs for this period - you either create mainly high-margin propositions people are willing to pay a lot for, like Apple, HTC or RIM, or you create a healthy mix of high and low-margin offers, and bet on volume, like Samsung, which might be on its way to become the Nokia that were.

Speaking of that, Samsung indeed declared a target to surpass Nokia as the world's biggest cell phone maker by 2014, and, looking at the pie charts below, displaying market share from 2007 to Q1 2011, it might arrive at the finish prematurely, although the market reaction to the full portfolio of Nokia Windows Phones next year is a big unknown.

Note, however, the huge increase of the “Others” category in Q1 of this year - the number of phones sold worldwide exploded with nearly 20% compared to Q1 2010, on account of companies like ZTE or Huawei, which are diligently assembling millions of handsets in the emerging markets, to commoditize the smartphone business too in the not so distant future.

Conclusion

All this power struggle resulted in a company like Apple with market capitalization second only to an oil giant like Exxon Mobil, with more than half of its revenue and the lion's share of profits due to the iPhone and iPad, whose popularity also peddled Apple's other creations.

The stock price has been stagnating this year worse since 2008, though. The ever forward-looking Wall Street recognized that it's been enough time for the competition to recover from the disruption knockdown Apple sent it into, and is starting to come up with answers of its own. This year has been huge for quality Android handsets, and next year we are expecting Microsoft to really enter the game with Windows 8 for tablets and its Nokia sidekick for phones.

Until the competition's efforts start really paying off, however, Apple will keep laughing all the way to the bank. It is one of the few American companies with high net cash deposits and no debt - the ultimate measure of success in the pre-”financial innovation” era. Its cash and equivalent holdings are expected to near $100 billion in a few quarters, enough to buy the whole cell phone making business outright, which would be silly, of course - by now Apple is most likely thinking of conquering a whole new segment, like TV business, for instance. What will be its future, though, and if it will become complacent like so many successful companies before, remains to be seen, especially with CEO Steve Jobs having to battle health issues and shying away from the daily grind.

Can Apple continue disrupting and innovating without "CEO of the decade" Steve Jobs at the helm of day to day operations? More so, without his constant internal drive to prove the Silicon Valley crowd that dismissed him once what Apple stands for? Wall Street doesn't think so, but its herd mentality has been wrong more often than Apple in the last few years, so we are bracing ourselves for a crazy mobile industry ride this year and the next. Phone Аrena will keep an eye on the financials of all the major players involved, and update them when new info comes out, so you can follow closely how things are unraveling.

Six-month unlimited plan is now 57% off

$90

$210

$120 off (57%)

Mint Mobile is now allowing you to get whichever plan you like for either three, six, or 12 months for just $15/mo. If you go for the six-month unlimited service, for instance, you'll now have to pay just $90 upfront instead of $210.

Daniel, a devoted tech writer at PhoneArena from 2010 to 2025, has been engrossed in mobile technology since the Windows Mobile era. His expertise spans mobile hardware, software, and carrier networks, and he's keenly interested in the future of digital health, car connectivity, and 5G. Beyond his professional pursuits, Daniel finds balance in travel, reading, and exploring new tech innovations, while contemplating the ethical and privacy implications of our digital future.

COMMENTS (20)

COMMENTS (20)

All comments need to comply with our

Community Guidelines

PhoneArena Community Rules

A discussion is a place, where people can voice their opinion, no matter if it

is positive, neutral or negative. However, when posting, one must stay true to the topic, and not just share some

random thoughts, which are not directly related to the matter.

Things that are NOT allowed:

Off-topic talk - you must stick to the subject of discussion

Offensive, hate speech - if you want to say something, say it politely

Spam/Advertisements - these posts are deleted

Multiple accounts - one person can have only one account

Impersonations and offensive nicknames - these accounts get banned

To help keep our community safe and free from spam, we apply temporary limits to newly created accounts:

New accounts created within the last 24 hours may experience restrictions on how frequently they can

post or comment.

These limits are in place as a precaution and will automatically lift.

Moderation is done by humans. We try to be as objective as possible and moderate with zero bias. If you think a

post should be moderated - please, report it.

Have a question about the rules or why you have been moderated/limited/banned? Please,

contact us.

![Verizon denies SpaceX is buying it [UPDATED]](https://m-cdn.phonearena.com/images/article/182254-wide-two_350/Verizon-denies-SpaceX-is-buying-it-UPDATED.webp)

![T-Mobile continues to experience major network issues across the nation [UPDATED]](https://m-cdn.phonearena.com/images/article/182238-wide-two_350/T-Mobile-continues-to-experience-major-network-issues-across-the-nation-UPDATED.webp)

Things that are NOT allowed:

To help keep our community safe and free from spam, we apply temporary limits to newly created accounts: