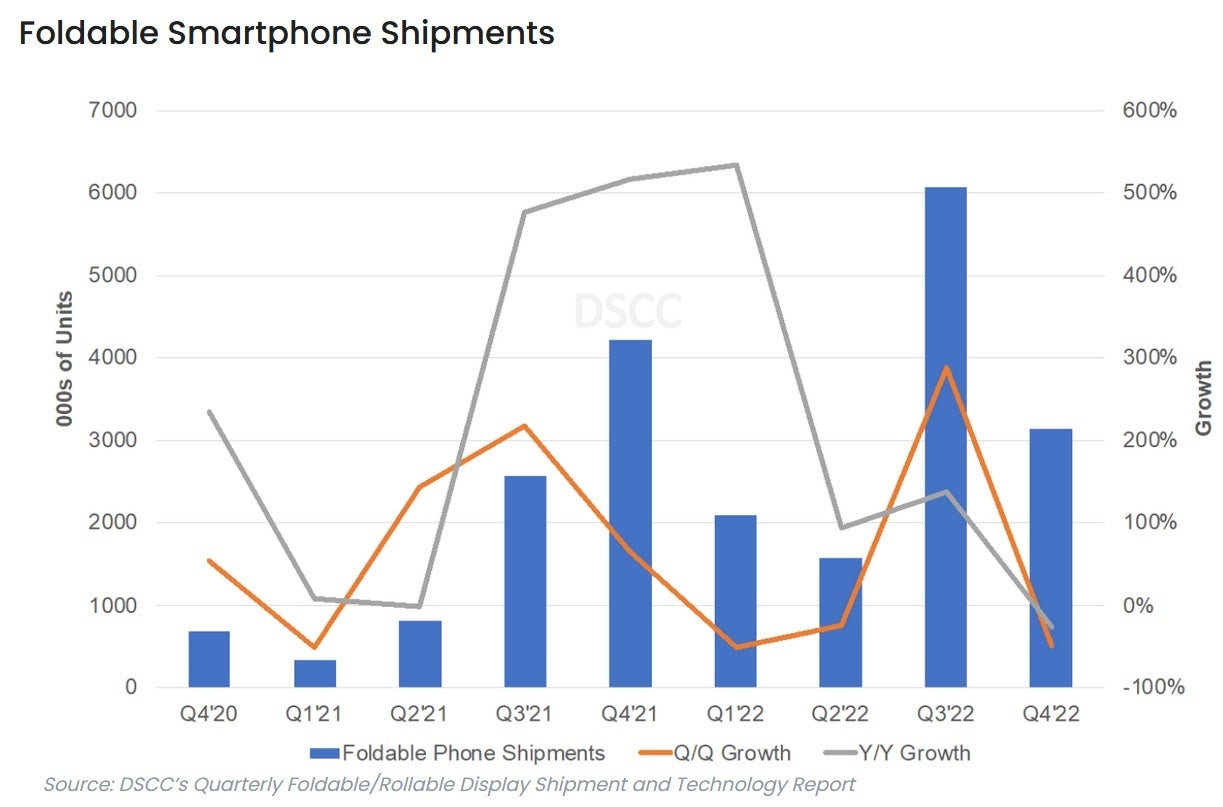

Global shipments of foldable phones suffered its first year-over-year decline during Q4

Ross Young is one of the most reliable tipsters around. He is co-founder and CEO of Display Supply Chain Consultants (DSCC) and today DSCC released some stunning news. Foldable smartphone shipments suffered through a rather tough 2022 fourth quarter as they dropped 48% compared to the third quarter, and 26% compared to the fourth quarter of 2021. 3.1 million foldable phones were delivered from the start of October 2022 through the end of December 2022.

Despite a weak fourth quarter, global shipments of foldable phones rose 62% in 2022

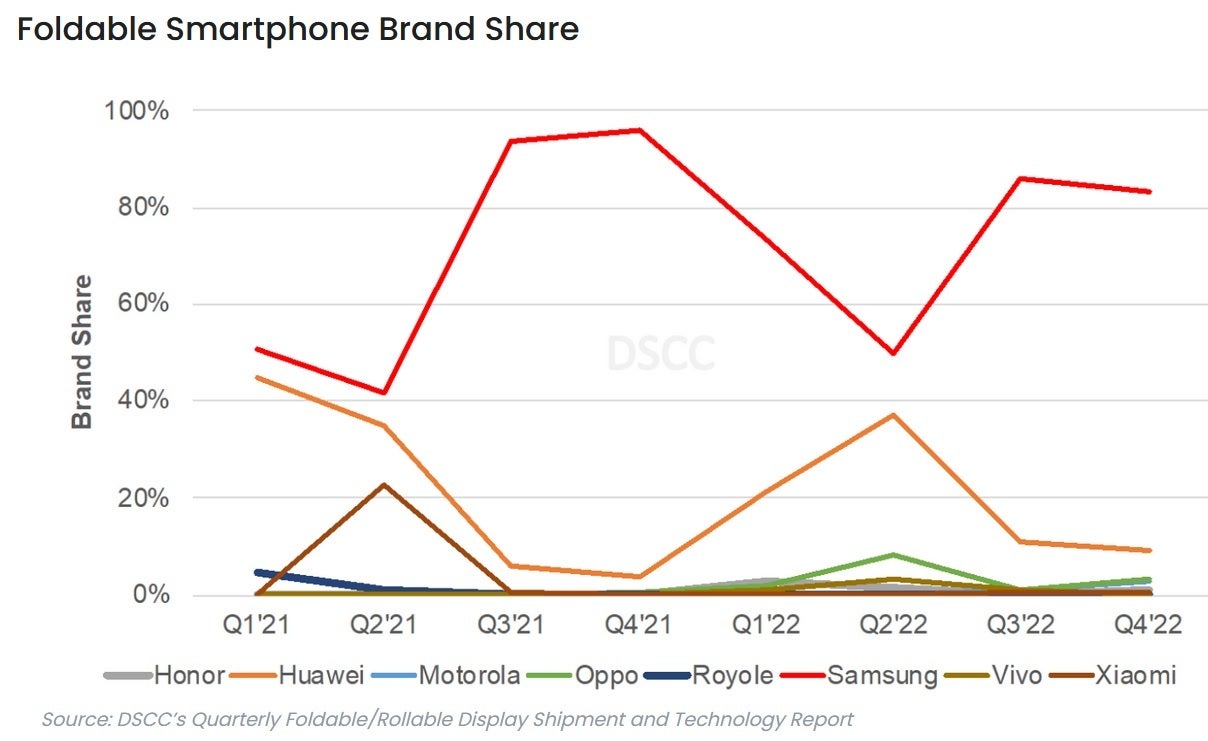

Despite the fourth quarter decline, for all of 2022 shipments of foldable handsets rose a strong 62% to 12.9 million units. Samsung remained on top of this space with a market share of 83%. That was down slightly from the third quarter's 86% and the 96% share of the foldables market that Sammy owned during the fourth quarter of 2021. The reason for the quarter-to-quarter decline was a sharp 50% drop in the company's foldable shipment volume during Q4 after it released the new Galaxy Z Fold 4 and Galaxy Z Flip 4 during Q3.

DSCC also noted that the fourth quarter of 2022 saw the recently released iPhone 14 series steal the spotlight from Samsung's foldables.

Samsung controls the global foldable phone market followed by Huawei and Oppo

The report says that fourth-quarter softness was apparent in the states where Samsung's share of foldable shipments was in the single digits. The top foldable phone worldwide during the fourth quarter of 2022 was the Galaxy Z Flip with a 47% slice of the global foldable smartphone pie. While the Galaxy Z Flip 4 maintained the top position that the Galaxy Z Flip 3 had during the same quarter in the previous year, the share owned by the clamshell declined from 52% during Q4 2021 to 47% during Q4 2022.

During the same period, the share of the global foldable market owned by the Galaxy Z Fold 4 was 28%. That was up slightly from the 27% share that the Galaxy Z Fold 3 earned during the fourth quarter of 2021. The third most shipped foldable model during the fourth quarter of 2022 was Huawei's clamshell Pocket S model with a 5% share of the global foldable market.

With Samsung as the top foldable phone manufacturer worldwide, Huawei was second followed by Oppo. The latter released the second-generation Find N2, and also launched its first clamshell model, the Find N2 Flip.

The soft trend in foldable shipments is expected to continue during the current quarter with RSCC looking for a 3% decline in year-over-year deliveries of foldable handsets worldwide. This trend should reverse in the second quarter of 2023 as new foldables are expected from Samsung (Galaxy Z Fold 5, Galaxy Z Flip 5) and Vivo. The latter and country-mate Oppo are expected to ship clamshell models to additional markets later this year at more affordable prices. As a result, total foldable shipments for the year should surpass 17 million units worldwide.

Samsung Display remains the top foldable display supplier with a vise-like grip on the market

In case you were wondering which display supplier leads in this niche area of the industry, we can give you a hint. They are headquartered in South Korea and the company name starts with an "S," ends with a "G," and has an amsun in the middle. Yes, Samsung Display was responsible for 81% of the foldable displays used during the fourth quarter of 2022, down from 91% during the third quarter of the year. For the quarter, Chinese supplier BOE saw its share rise from 4% during Q3 to 17%.

Shipments of foldable phones worldwide was weak during the fourth quarter

For all of 2022, Samsung Display led the way as it supplied 82 out of every 100 foldable handsets (that's 82% for those who hate doing math) while BOE snagged 13% of the business. So both firms have a pretty good headlock on the market combining for a market share of 95%. Technically, this is a duopoly even though Samsung still accounts for the lion's share of the business. And DSCC expects to see Samsung maintain or grow its share of foldable display shipments in 2023.

Overall, foldable panel shipments rose 53% in 2022 to 15.2 million units. Further growth is forecast this year with DSCC calling for such deliveries to exceed 20 million units in 2023.

Popular stories

Latest News

Things that are NOT allowed:

To help keep our community safe and free from spam, we apply temporary limits to newly created accounts: