One of T-Mobile’s announcements that made waves from yesterday’s press event was JUMP!, the “un-carrier’s” new upgrade program that allows subscribers to upgrade their hardware with the latest and greatest twice per year.

It amounts to a trade-in really, and you do have to pay for the privilege, $10 extra per month, which also includes total equipment coverage against damage to the device, malfunctions, loss or theft. How do the numbers wash out though? Is it a good deal? We will give you some examples and run through the basic math.

The way the program works is not very complicated. Once you have been enrolled in the JUMP! program for 6 months, you can upgrade to a new phone using the same financing arrangement that exists with T-Mobile’s Equipment Installment Plan (EIP) for new or eligible customers. For those that do not understand how the EIP works, here is the rundown:

In lieu of subsidies and a contract, T-Mobile separates the equipment from the service completely. When you activate service, you can buy your device at full retail or make a down payment and make 24 equal payments. You mobile service is a separate payment (on the same bill). Yourdown payment may vary based on your credit score. Arguably, the result is the same as a two-year service agreement, but we are not going to get into that right now.

Recommended For You

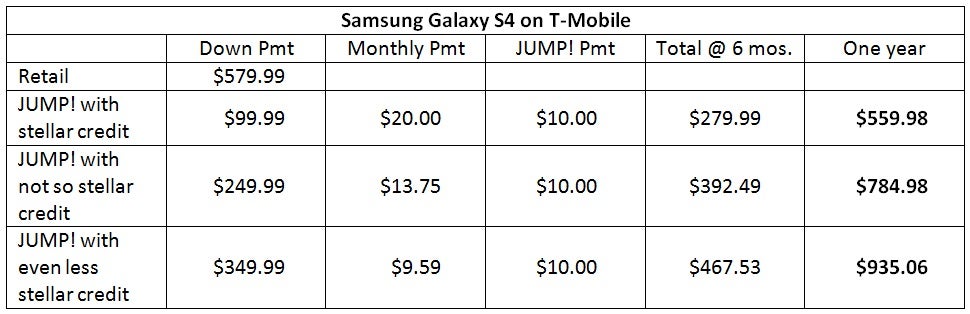

We will use the venerable Samsung Galaxy S4 for our example. We are not including the mobile service fees or any applicable taxes since they vary state by state. Under normal circumstances, “well qualified buyers” would make a down payment of $99.99 and then make 24 equal monthly payments of $20 which equals the retail price of $579.99.

With the JUMP! upgrade plan, you pay an extra $10 per month for the privilege of upgrading your equipment a couple times per year. $99.99 down, plus $30 per month for six months equals $279.99 spent on equipment by the time you are eligible to upgrade. Assuming you upgrade to a device of equal standing, you would trade-in your well-cared-for device then pay another $99.99 down for a new one and continue on your way making payments of $30 per month. $279.99 spent over a period of six months and being able to upgrade at that kind of preferred pricing is not a terrible option at all. For the year, you could end up paying $559.98 for two new phones which is less than full retail for a single new device, or in this case, a new Galaxy S4.

What if you are not a “well qualified buyer?” Well, your initial down payment for the equipment is higher, but that is offset by lower monthly payments. Let us assume that your credit is not stellar and T-Mobile requires a down payment for an SGS4 of $249.99. That would leave 24 equal payments of $13.75 for the equipment, plus $10 for JUMP! $249.99 plus a combined $142.50 over six months equals $392.49 spent in six months, or $785 per year.

How about someone with credit in the dumpster? How about a big down payment of $349.99 which leaves 24 equal payments of $9.59 per month, plus $10 for JUMP! Over a six month period, it adds up to $467.53, or $935 per year. We have outlined the costs in the table below. With exception of the "well qualified" rates, we picked the potential down payments at random, but the math itself clearly works since T-Mobile's EIP does not charge an interest rate (0% APR).

Our example does not take into account changes that might occur with a customer's credit rating, but you can count on T-Mobile conducting a check at each time you want to upgrade your device. Also, our example touches on similar price schemes for similar devices. The cost structure obviously goes up if the change were being made from a Galaxy S4 to an Apple iPhone 5, or from an LG Optimus L9 to an HTC One.

In the final analysis, JUMP! is going to be a great option for people with a good credit score and extra money to spend. However, if you are on a tighter budget, or have bruised credit, it is a good idea to examine other options if you like to replace your gadgets often.

Get Visible as low as $20/mo for 1 year. Limited time offer with code: FRESHSTART

$20

/mo

$25

$5 off (20%)

Offer Ends 6.1.2026 at 11.59pm ET. New members get $5/mo off the $25/mg Visible plan, $35/mo Visible+ plan, or $45/mo Visible+ Pro plan for the first 12 months. Promo code FRESHSTART required at checkout.

Maxwell Ramsey has made significant contributions to PhoneArena through his detailed reporting on technology policy and advancements, such as wireless charging standards and FCC regulations, helping demystify complex topics for a broad readership.

Recommended For You

COMMENTS (16)

COMMENTS (16)

All comments need to comply with our

Community Guidelines

PhoneArena Community Rules

A discussion is a place, where people can voice their opinion, no matter if it

is positive, neutral or negative. However, when posting, one must stay true to the topic, and not just share some

random thoughts, which are not directly related to the matter.

Things that are NOT allowed:

Off-topic talk - you must stick to the subject of discussion

Offensive, hate speech - if you want to say something, say it politely

Spam/Advertisements - these posts are deleted

Multiple accounts - one person can have only one account

Impersonations and offensive nicknames - these accounts get banned

To help keep our community safe and free from spam, we apply temporary limits to newly created accounts:

New accounts created within the last 24 hours may experience restrictions on how frequently they can

post or comment.

These limits are in place as a precaution and will automatically lift.

Moderation is done by humans. We try to be as objective as possible and moderate with zero bias. If you think a

post should be moderated - please, report it.

Have a question about the rules or why you have been moderated/limited/banned? Please,

contact us.

Things that are NOT allowed:

To help keep our community safe and free from spam, we apply temporary limits to newly created accounts: